|

|

|

May 2012

• • • • • • • • • • • • • • • • •

| |

• • • • • • • • • • • • • • • • • • • • • • • • • • •

"With both the larger regionals as well as smaller community banks having improved outlooks, head count reduction initiatives of past years have been replaced by active hiring from entry level to senior manager levels," As quoted in The Birmingham News

April 21, 2012 | |

|  Featured Article Featured Article | |

|

As Job Market Improves, Candidates Notice

In the depths of the recession, as unemployment rates were rising and everyone knew someone who was being affected, “It’s better than no job at all” became a common refrain across the factory floors and offices of America. While it was a poor retention strategy, it was a worse recruiting strategy and now, with the economy on the mend, candidates are no longer falling for it.

“Candidates now know—as much, if not more than hiring managers—that the market is improving,” says Rob Romaine, president of MRINetwork. “Top candidates are getting multiple offers, and those who don’t like what they hear from one employer are more frequently willing to wait for another suitor.”

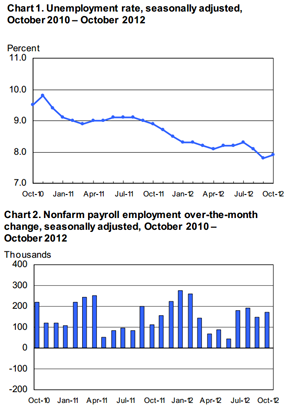

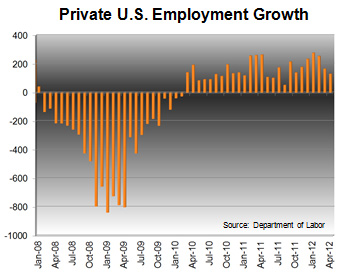

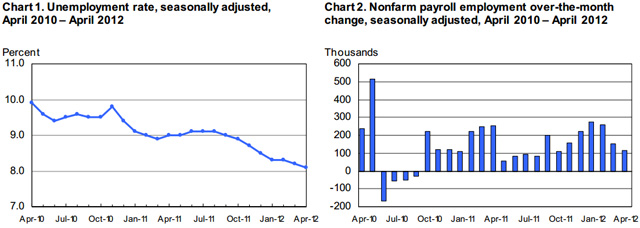

Employment growth was below expectations in March, with just 120,000 positions added compared to more than 200,000 in some projections. Though that had followed four months in which more than a million positions were added collectively. The rate of growth is expected to remain decidedly slower for the remainder of the year. But, short of the U.S. economy slipping back into to a major recession—something almost no economist is projecting—the labor market is going to remain competitive. Employment growth was below expectations in March, with just 120,000 positions added compared to more than 200,000 in some projections. Though that had followed four months in which more than a million positions were added collectively. The rate of growth is expected to remain decidedly slower for the remainder of the year. But, short of the U.S. economy slipping back into to a major recession—something almost no economist is projecting—the labor market is going to remain competitive.

“It’s dangerous to underestimate the competitiveness of the labor market. Companies are pursuing plans, bidding on business, and making projections, only to later realize that it is taking many months for their internal HR departments to fill the roles and often at higher starting salaries than expected,” notes Romaine.

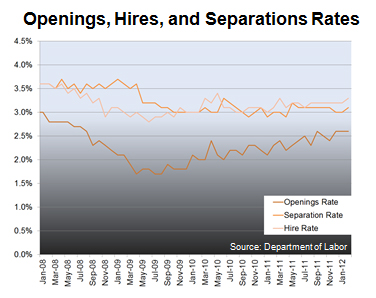

The job openings rate has risen from 1.8 percent in the worst of the recession to 2.5 percent in February. Over the same time, the hires rate has risen from 2.8 to 3.3 percent, while the separations rate has fallen from 3.5 to 3.1 percent. While the positions available and being filled span almost all sectors of the economy, the bulk of employees being hired share one thing in common: four-year college degrees.

Since March of 2011, total employment by those with a Bachelor’s degree or higher has risen by more than 1 million positions. Total employment by those with less than a Bachelor’s degree, though, has actually shrunk by 218,000 positions. The unemployment rate for those in management, professional, and related occupations has fallen to 4.2 percent, and when you look at more technical fields, the rate begins to approach full employment.

“Candidates have realized how rare a commodity they are, but when an employer isn’t making them feel courted, somebody else will,” says Romaine. “It’s not that top performers are demanding the red carpet treatment during the hiring process, but when they have multiple offers, the style of the process can be as important as the substance of the opportunity.”

| |

| Notable Global Events | |

|

The euro zone’s unemployment rate continued to rise in February, reaching 10.8 percent. A proposal in front of the European Commission is suggesting cutting labor taxes while raising use taxes to spur employment growth. The euro zone’s unemployment rate continued to rise in February, reaching 10.8 percent. A proposal in front of the European Commission is suggesting cutting labor taxes while raising use taxes to spur employment growth.

The Bank of Korea recently lowered its GDP growth projections for 2012 from 3.7 to 3.5 percent with a statement tying the downgrade to projected euro zone contractions. Unemployment in South Korea, though, was down to 3.4 percent in March from 3.7 percent a month earlier.

| |

| Spotlight on Chile | |

|

Retail Demand Replaces Commodities

Throughout the recession, Chile has been able to temper the drops in the global economy with the rising demand and price of copper—a resource of which Chile is the world’s largest producer. With the global economy still wobbling, seeing a decrease in demand for copper should have signaled the beginning of a slowdown in the country, and, while that may still happen, it hasn’t yet.

In March 2012, total copper production fell 2.6 percent from a year earlier, while other natural resources like wood and oil fell even further to 7.7 and 13.9 percent respectively. Yet, Chilean consumers seemed to move in the opposite direction, causing consumer sales to surge in retail and supermarkets. Retail sales have risen as much as 9.2 percent from a year ago, despite five separate interest rate increases last year targeted at slowing domestic demand.

While manufacturing has also slowed, economists expect the Chilean central bank to continue to raise interest rates in light of continued consumer demand.

Inflation in Chile has remained high throughout the global recession, despite briefly slipping into negative growth itself, in large part because of the rising price of copper. In February, the annual inflation rate had reached 4.4 percent, though it declined to 3.8 percent in March.

Chile’s GDP is expected to grow between 4 and 5 percent in 2012 after a robust 6 percent growth in 2011.That growth has helped push down its unemployment rate, which has fallen to 6.6 from 7.3 percent a year earlier. While 6.6 percent unemployment is low compared to many developed economies today, Chile’s Finance Minister Felipe Larrain has gone on record calling the falling rate “near full employment.”

In comments related to a Chilean bond issuance in late April, Larrain highlighted the unemployment rate and said the government is aiming to increase labor-force participation, especially among women, as the economy continues to grow.

It was a sentiment echoed by a Goldman Sachs Group economist in an email to investors, which reported that Chile’s “labor market remains tight,” and that “the economy is operating at around full employment.”

In the coming months, eyes will turn toward Chilean manufacturing numbers to see if the retail spike is going to translate into more production. Should the domestic market continue to remain strong, it should help to counteract a seasonal rise in unemployment going into the summer months.

| |

| Spotlight on New Mexico | |

| Boosting Private Industry

When an extraterrestrial flying saucer crashed in the desert outside Roswell, New Mexico, in the summer of 1947, its landing was clearly impeded by the lack of proper spaceport facilities in New Mexico—or anywhere on Earth for that matter. Over the last several years, the State of New Mexico has been working to rectify that deficiency by constructing Spaceport America, the country’s first commercial space launch and recovery facility.

The spaceport is a very small, albeit glamorous, part of a concerted effort by New Mexico to expand private industry and employment in a state where nearly one in four workers are employed by the government. Nationally, the average is less than one government employee for every six workers.

“Trying to change the balance between the public and private economies is something governors in New Mexico have been struggling with for 25 years,” says Paula Ancona, Managing Partner of Management Recruiters of the Sandias outside of Albuquerque. “Since Governor Susana Martinez took office, though, expectations have been higher than ever before. She has already helped to bring hundreds of new, high-paying technology jobs to New Mexico, and in a state the size of ours, that’s a meaningful amount.”

A sizable part of the government presence in New Mexico is from high-tech scientific, defense, and research-related roles. The Los Alamos National Laboratory, established by Robert Oppenheimer as the home for the Manhattan Project, employs more than 9,000.

Ancona notes though that in many of the non-scientific positions she places in the state, there is a limited pool of talent with private sector experience. Candidates frequently have to be sourced from surrounding states, if not farther away, making filling more specialized roles even more difficult.

“Intellectually, hiring managers understand tight the market is. They’ll say they know the candidate they are looking for might not exist. Yet, they’ll still hold out for that pedigree, while passing on world-class talent without so much as an interview,” says Ancona. “The attitude is that if they’ve got time to keep looking, they’ll take it.”

That perception might not be all wrong. While many Western states—Nevada and California for example—saw economic bubbles that burst in the last few years, New Mexico never had the same level of buildup. Then again, with such a large concentration of professional-level government and government-related employment, they also didn’t take the hit that others did.

“Companies are especially looking to add roles along the lines of business development positions,” notes Ancona. “But it’s measured growth, and cautious decisions are being made with a heavy eye on quality—quality of product, quality of services and consequently, quality of talent.”

| |

|

|

|